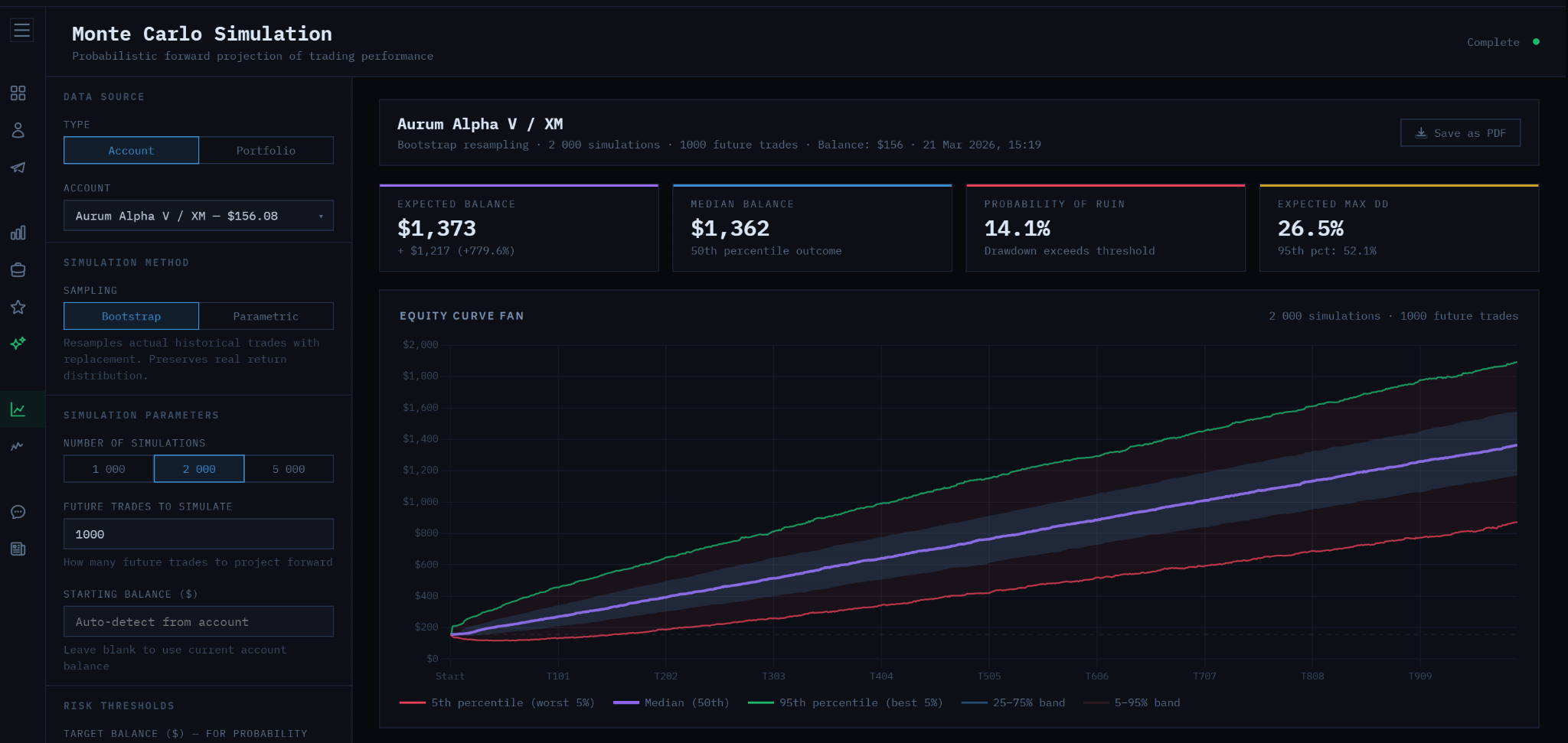

We are pleased to announce the addition of Monte Carlo Simulation to the FX-Monitor analytics module.

This new feature expands the platform’s analytical capabilities by providing a probabilistic view of strategy performance and risk. Instead of relying only on historical backtest curves or a single sequence of trades, Monte Carlo Simulation helps traders evaluate how a system may behave under many alternative scenarios.

What Monte Carlo Simulation Does

Monte Carlo Simulation is a statistical modeling method that repeatedly generates new possible outcomes based on historical trading data.

In practical terms, the system takes the existing trade history and runs hundreds or thousands of randomized simulations. Depending on the selected method, it can resample actual trades or model returns statistically in order to estimate a distribution of future outcomes.

This makes it possible to move beyond a single backtest line and examine a full range of potential results.

Why It Matters

A standard backtest shows only one path — the exact historical sequence of trades that occurred in the data.

However, real trading rarely unfolds in the same order or under identical conditions.

Monte Carlo Simulation helps answer more realistic questions such as:

- How sensitive is the strategy to randomness in trade sequencing?

- What range of balances is realistically possible in the future?

- How severe could drawdowns become under less favorable conditions?

- What is the estimated probability of ruin or breach of risk thresholds?

- Is the strategy robust, or does it rely too heavily on one “ideal” path?

This makes Monte Carlo analysis especially valuable for traders who want to evaluate not only profitability, but also stability, resilience, and risk exposure.

Key Benefits

With the new Monte Carlo module, users can:

- Estimate expected and median future balance

- Analyze worst-case and best-case outcome ranges

- Measure probability of ruin

- Evaluate expected maximum drawdown

- Compare confidence bands across large numbers of simulations

- Test how a strategy behaves when historical trade sequences are disturbed by randomness

This provides a much deeper understanding of whether a system is genuinely robust or simply benefited from a favorable historical sequence.

Available Simulation Options

The module includes flexible settings for analysis, including:

- Account or Portfolio as the data source

- Bootstrap and Parametric simulation methods

- Adjustable number of simulations

- Custom number of future trades to project

- Optional starting balance settings

- Risk thresholds for forward probability analysis

These controls allow traders to tailor the simulation to their own evaluation process and risk framework.

A More Realistic Way to Evaluate Risk

One of the main advantages of Monte Carlo Simulation is that it shifts the focus from “how good the backtest looks” to how the strategy may behave under uncertainty.

This is particularly important for:

- portfolio construction,

- system comparison,

- prop firm preparation,

- capital allocation decisions,

- and long-term robustness analysis.

In other words, Monte Carlo Simulation helps traders evaluate not only whether a strategy worked in the past, but whether it can remain viable under changing and imperfect future conditions.

Now Available in FX-Monitor

Monte Carlo Simulation is now available inside the FX-Monitor analytics section as part of the ongoing platform expansion.